The structure of the investment process and its functioning:

The investment process brings together suppliers who have excess funds and demanders who need funds. Households, governments, and businesses are the main participants in the investment process, and each of these participants may act as a supplier or a demander of funds at different times. Typically, Households who spend less than their income have savings, and they aim to invest those surplus funds to generate a return. Consequently, Households are usually net suppliers of funds in the investment process. On the other hand, governments usually spend more than they collect through tax revenue, so they use instruments such as bonds and other debt securities to obtain additional funds. This means that governments are typically net demanders of funds. Businesses usually need to raise funds to finance new investments and other operations, so They may issue debt or equity securities. Therefore, this makes businesses net demanders of funds most of the time. Overall, the investment process is a way for individuals or entities with excess funds to gain a return on their investments and for those who require funds to obtain the necessary capital to carry out their objectives.

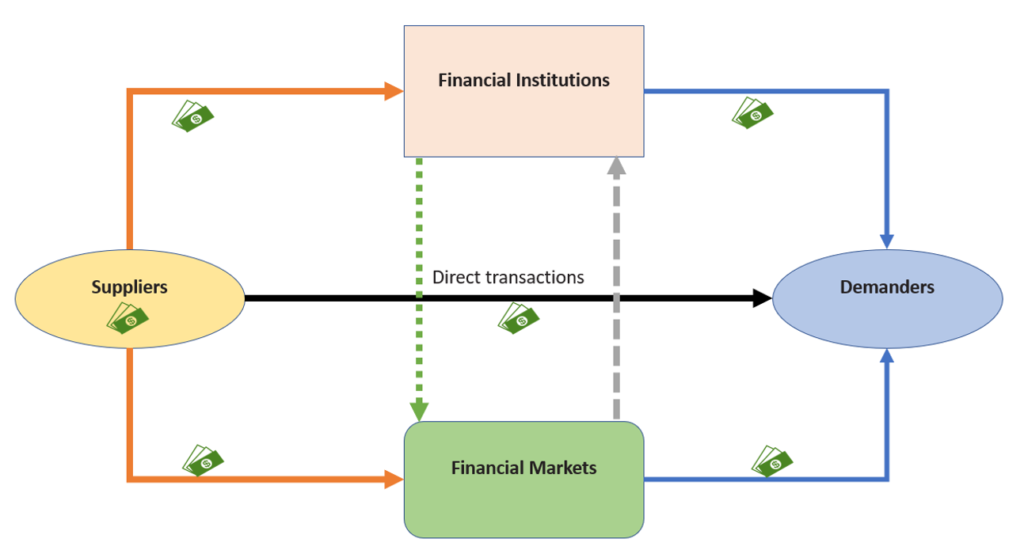

Suppliers and demanders of funds often meet through a financial institution or a financial market. Financial institutions such as banks and insurance companies pool the resources from households and other savers, using funds to provide loans and invest in securities like bonds issued by the government. Financial markets, on the other hand, are markets where suppliers and demanders of funds trade financial assets, typically with the assistance of intermediaries like brokers and dealers. Various forms of investments, such as stocks, bonds, commodities, and foreign currencies, trade in financial markets.

What is the securities market?

The securities market is the predominant financial market in the United States, it includes stock markets, bond markets, and options markets. These markets also exist in most of the world’s major economies. Prices of securities traded in these markets are established by the forces of interactions between buyers and sellers, just like other prices are set in different types of markets. For example, if the number of investors who want to buy Tesla shares is greater than those who want to sell, the price of Tesla’s stock will increase. As investors receive new information about the company, changes in supply (investors who want to sell) and demand (investors who want to buy) may result in a new market price.

What is the role of financial markets?

Financial markets facilitate the process of bringing together buyers and sellers by minimizing transaction costs. Additionally, financial markets provide another valuable function by establishing market prices for securities, which can be easily tracked by market participants. For instance, a firm launching a new product may get an initial response indication of how that product will be received in the market by observing whether investors increase or decrease its firm’s stock price upon learning about the new product. It’s important to note that the suppliers of funds can transfer their resources to the demanders through financial institutions, financial markets, or direct transactions. Financial institutions can function in financial markets as either suppliers or demanders of funds, as shown by the broken lines. For the economy to grow and prosper, funds must be channeled to those with attractive investment opportunities. If individuals decide to hoard their extra funds instead of investing in financial institutions and markets, then organizations in need of funds may struggle to obtain them. As a result, government spending, business expansion, and consumer purchases would decline, ultimately slowing down the economy.

The difference between individual investors and institutional investors:

When households have extra funds available to invest, they must decide to personally handle their investment decisions themselves or delegate some or all of that responsibility to professionals. This creates an important distinction between two types of investors in the financial markets. Individual investors manage their own funds to reach their financial goals, such as earning returns on idle money, building a retirement income, and providing security for their families. Individuals who lack the time or knowledge to make investment decisions often employ institutional investors—investment professionals and experts that earn a living by managing other people’s money. These professionals or institutional investors trade significant amounts of securities for individuals, as well as for businesses and governments. Institutional investors are various entities such as banks, life insurance companies, mutual funds, pension funds, and hedge funds. To illustrate, a life insurance company invests the premiums it collects from policyholders to generate returns that will cover death benefits paid to beneficiaries. Both individual and institutional investors utilize comparable fundamental principles when deciding how to invest money. Nevertheless, institutional investors typically control larger sums of money and have more advanced analytical skills than most individual investors.

Risk management strategies:

Risk management strategies are vital tools for investors seeking to protect and optimize their investments. These strategies are designed to mitigate potential financial losses and improve the overall performance of investment portfolios. We’ll explore various risk management strategies that you can implement to safeguard and enhance your investments:

Equal-weighting:

One popular approach to risk management is equal weighting, where investors allocate the same amount of capital to each asset within their portfolio. This strategy inherently promotes diversification, spreading the risk equally across all holdings. By doing so, investors reduce the potential impact of a single asset’s poor performance on the overall portfolio. This ensures that no single investment dominates the risk profile, creating a more stable and balanced portfolio.

Stop-Loss orders:

Another effective risk management strategy is the implementation of stop-loss orders. These orders allow investors to set predetermined price levels at which they are willing to sell an asset to limit potential losses. By utilizing stop-loss orders, investors establish a safety net that helps protect their capital in the event of significant market downturns or adverse price movements.

Sector diversification:

Sector diversification is a risk management strategy in a portfolio that involves spreading investments across different industry sectors. This approach aims to reduce risk by minimizing the impact of poor performance in any single sector on the overall portfolio. Diversifying across sectors can help protect against sector-specific downturns and capitalize on growth opportunities in various areas of the economy.

Author

Hi, I’m Mason! My mission is to make finance accessible and fun for everyone. I love breaking down things that seem difficult into simple, easy, and useful tips that help you make good decisions. My aim is to ensure your experience on our blog is informative and fun.

View all posts